This week we're going to review OPEC's August Oil Market Report (covering July OPEC & global oil data). As you’ll see, it shows there was a large shortfall in the amount of oil produced in July, a story that doesn’t seem to be being told elsewhere, as even the analysts don’t read the entire report (100+ pages)

Wednesday's release of US oil data for the week ending July 15th by the US Energy Information Administration indicated that our oil imports rebounded back to above recent averages, that our refineries ramped back up to seasonal levels to use all of those extra imports, and as a result another small portion of our monstrous glut of crude oil was converted into a glut of refined products.

A number of on again, off again, stories that Russia was planning to meet with the members of the OPEC cartel to negotiate production cuts drove oil prices higher last week, but even now it's still not clear if there was any actual communication between any leaders of the countries to bring about such a meeting

Nowadays the energy picture is confusing at best as the more information we are shown the more blurred our vision seems to become. Mixed messages, poor reporting and a media hungry to sensationalize anything it thinks can grab a headline have led to many wondering what the true energy situation is. We hear numerous reports on how the shale revolution will transform the energy sector, why alternatives are just around the corner, why advances in oilfield extraction techniques and new finds will help to lower oil prices. Yet no sooner have we read these rosy reports than we are bombarded with negative news on the Middle East, on why alternatives will never compete, on peak oil and declining oil production.

So where do we really stand? Is our energy future one of falling prices and plentiful supply or should we prepare for declining supply and sky high prices?

How much are you paying to fuel Wall Street oil speculators? A new, very timely St. Louis Federal Reserve research paper, Speculation in the Oil Market finds 15% of oil price increases are due to speculation and is the second most powerful mover of prices beyond actual physical demand. Demand itself accounts for 40% of the total oil price increase.

Déjà vu, it's 2008 all over again. Why are gas prices soaring through the roof?

Some are revisiting oil speculation as the culprit. Commodity futures speculation always pops up in the public discourse the minute gas prices go above $3.65, yet nothing ever seems to come of it.

Our usual stupid political tricks, from tapping the strategic oil reserve to the GOP blaming Obama for gas prices, are in full swing. Isn't this all getting rather old? Wouldn't we all just like a stable price fluctuation in a key critical commodity upon which our economy and our empty pockets depend?

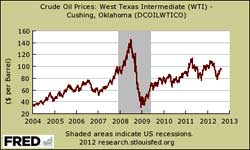

We know one thing, $5 gas can literally kill economic recovery. Oil shocks are correlated to recessions, as James Hamilton points out as do others. Below is a quarterly historical graph of real GDP percent change vs. the West Texas Intermediate average Oil Price. Notice the spikes in oil price and the grey recession bars.

Sorry speculative traders in commodities, the Fed actually did a just say no on more quantitative easing. The FOMC meeting minutes for January 24-25th were released last week and some speculative commodities traders still seem to be in denial land.

The FOMC money quote:

The Committee also stated that it is prepared to adjust the size and composition of its securities holdings as appropriate to promote a stronger economic recovery in a context of price stability. A few members observed that, in their judgment, current and prospective economic conditions--including elevated unemployment and inflation at or below the Committee's objective--could warrant the initiation of additional securities purchases before long. Other members indicated that such policy action could become necessary if the economy lost momentum or if inflation seemed likely to remain below its mandate-consistent rate of 2 percent over the medium run. In contrast, one member judged that maintaining the current degree of policy accommodation beyond the near term would likely be inappropriate; that member anticipated that a preemptive tightening of monetary policy would be necessary before the end of 2014 to keep inflation close to 2 percent.

A new year, a new day and a flurry of economic and financial predictions. Who are we to buck the trend? Yet, buck the trend we shall. While many news articles claim jobs will appear in 2012 and the economy is on the mend, uh, we don't think so. What we have is America stuck in a Labrea tar pit of bad policy and a never ending middle class head shrink.

Welcome to the weekly roundup of great articles, facts and figures. These are the weekly finds that made our eyes pop.

China iPhone Manufacturer Foxconn's Horrific Working Conditions

Think the iPhone is made in America? Like most things these days, manufacturing is offshore outsourced to China. Out comes another report on the terrible working conditions at the iPhone/iPad factory.

How much are you paying to fuel Wall Street oil speculators? A new, very timely St. Louis Federal Reserve research paper,

How much are you paying to fuel Wall Street oil speculators? A new, very timely St. Louis Federal Reserve research paper,

Sorry speculative traders in commodities, the Fed actually did a just say no on more quantitative easing. The

Sorry speculative traders in commodities, the Fed actually did a just say no on more quantitative easing. The  A new year, a new day and a flurry of economic and financial predictions. Who are we to buck the trend? Yet, buck the trend we shall. While many news articles claim jobs will appear in 2012 and the economy is on the mend, uh, we don't think so. What we have is America stuck in a Labrea tar pit of bad policy and a never ending middle class head shrink.

A new year, a new day and a flurry of economic and financial predictions. Who are we to buck the trend? Yet, buck the trend we shall. While many news articles claim jobs will appear in 2012 and the economy is on the mend, uh, we don't think so. What we have is America stuck in a Labrea tar pit of bad policy and a never ending middle class head shrink.

Recent comments