The November personal income and outlays report shows a 0.5% change in consumer spending, even when adjusted for inflation. This is the highest monthly percentage change in consumer spending adjusted for inflation since February 2012 and is good news for Q4 GDP. October consumer spending was revised up to 0.4% for the month. Personal income didn't fare as well and not adjusted for inflation increased 0.2%. The rise in consumer spending is another indicator the economy might be picking up.

Consumer spending is another term for personal consumption expenditures or PCE. November's PCE is higher than all of Q3 and assuming December consumer spending stays strong, implies PCE would be much above 3 percentage points of GDP growth. Real personal consumption expenditures were an annualized $10,868.2 billion. Q3 Real GDP was $15,839.3 billion which shows consumer spending is about 68% of GDP and critical to U.S. economic growth. Real means adjusted for inflation and is called in chained 2009 dollars

The change is so great, even without any consumer spending growth in December, PCE has already doubled from what Q3 was, $100 billion vs. $52.3 billion for Q3. This implies consumer spending will be at least 2.8 percentage points of Q4 GDP and the odds of PCE being zero or negative in December are next to nil from all other economic indicators. In other words, expect PCE to be much higher than a 2.8 percentage point contribution to Q4 GDP. That said, we expect inventories to change negatively after the whopping Q3 build up, although those monthly figures are not yet released and we'll calculate out those estimates separately in other overviews.

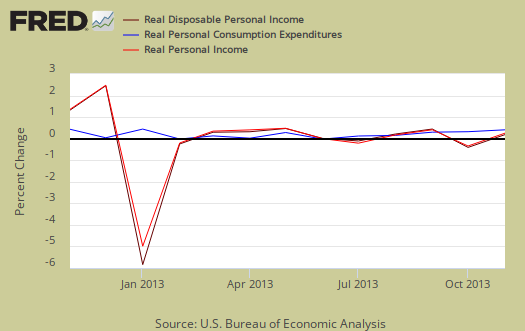

Disposable income is what is left over after taxes and increased 0.1%, even when adjusted for prices for inflation was so low in November. Disposible income shrank -0.2% in October. Graphed below are the monthly percentage changes for real personal income (bright red) which increased 0.2% for the month, real disposable income (maroon) and real consumer spending (blue).

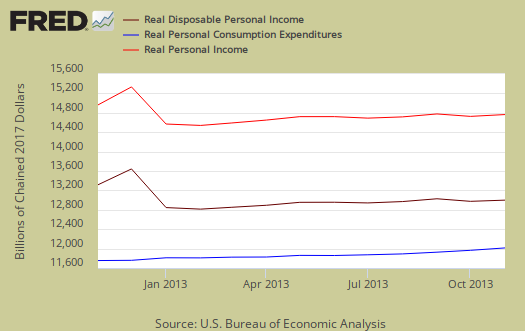

Below are the real dollar amounts for real personal income (bright red), real disposable income (maroon) and real consumer spending (blue) for the last year.

Consumer spending encompasses things like housing, health care, food and gas in addition to cars and smartphones. Most of PCE is most about paying for basic living necessities, known as services, vs. durable consumer goods. Graphed below is the overall real PCE monthly percentage change so one can see the monthly increases in comparison to past months.

For November, durable goods spending blew out the charts. Real durable goods had the highest monthly increase since October 2010. Below are the real monthly percentage changes and services also showed an increase in spending.

- Durable goods: +2.2%

- Nondurable goods: 0.0%

- Services: 0.4%

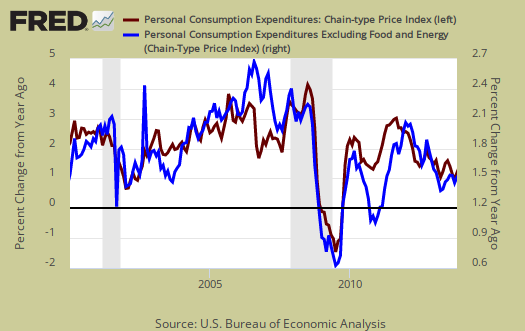

Price indexes are used as divisors to adjust for inflation and price changes. The indexes are used to compute spending and income for an apples to apples, real dollar comparison to previous months and years. Economic statisticians use real dollars so one does not erroneously assume economic growth when the increase is really just inflation. The price index had no change, for the past two months. The price index is now up only 0.9% from a year ago. Minus energy and food, the price index increased 0.1% from last month and is up 1.1% from this time last year. This is an incredibly low rate of inflation and well below the Fed's 2.0% target rate. While the PCE price index represents inflation, it is different from CPI.

Graphed below is the PCE price index, in red, scale on the left, and the PCE price index minus food and energy in blue, scale on the right. This is the percent change from one year ago. We are seeing low inflation similar to the deflationary period of 2008, caused in part by the Great recession and a massive drop in global economic demand. For those watching quantitative easing, you might take a look at this article on the Fed's concern for potential deflation.

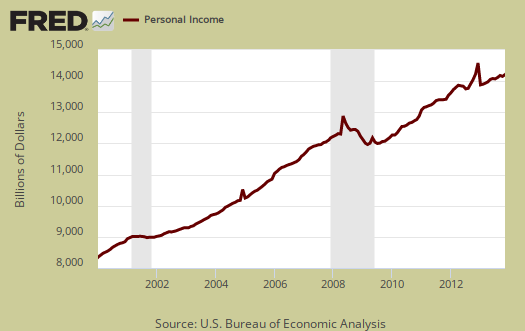

Personal income is total income, from all sources, for everybody in the United States who reported and are not part of the underground economy. Below is personal income, not adjusted for inflation, or price changes and the news even on aggregate isn't good like spending is.

The BEA reports real personal income as real personal income minus transfer receipts. This is government payments, such as social security, removed and also adjusted for inflation. Here too we see no change for the month. This graph shows how much personal income increased that wasn't funded by the government and is used as a recession indicator as show in the below graph with the gray bars indicating recessions. Transfer receipts are payments from the government to individuals where no actual services (work) was performed. This includes social security, unemployment insurance, welfare, veterans benefits, Medicaid, Medicare and so on.

Disposable income is what is left over after taxes. DPI increased 0.1% from last month, yet decreased -0.2% for October. DPI adjusted for inflation (see the price indexes above), increased 0.1%, from the previous month. These numbers are aggregates, which includes income of the uber-rich, or the 1% of the population, as they are now called. Below is DPI by levels.

Taxes collected on person income took a chunk and increased $14 billion from last month and the previous month increased $13.8 billion. Below is a graph of personal income taxes where one can also see the effect of the Bush tax cuts as well as the recession (no income, no taxes on that income), as well as the temporary tax breaks from the Stimulus.

Graphed below is real disposable income per capita. Per capita means evenly distributed per person and population increases every month. While income in the U.S. grows so does the population which earns that total pot of income. November mid-month the U.S. population was 317,412,000. What we see when taking increased population into account, we basically have no growth in real disposable personal income over the years. Notice how real disposable income per person really started to flatline in 2000. That's just when offshore outsourcing to China started in earnest. The great recession has made the situation much worse.

Wages and Salaries showed signs of life as they increased 0.4% from last month. Overall employment compensation increased 0.3% as supplements to wages only increased 0.2% for the month Yet lord protect investors as dividends increased 0.7% for the month. Assets are Wall Street income, which most of America doesn't have of which dividends are a part and overall increased 0.3% Rental income increased 0.3% for the month.

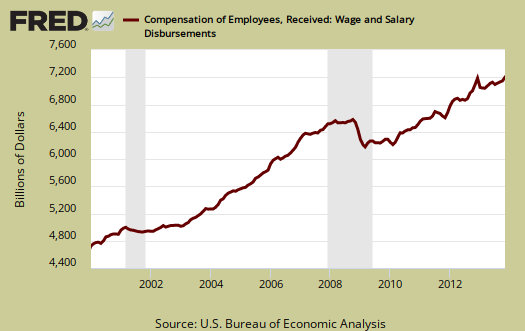

Graphed below are wages and salaries for the past decade. Notice the dip and the more flat line than earlier in the decade. Bear in mind these are aggregate, or all wages and salaries, and not adjusted for inflation. nbsp;From the report:

Private wages and salaries increased $26.1 billion in November, compared with an increase of $9.9 billion in October. Goods producing industries' payrolls increased $8.3 billion, compared with an increase of $1.4 billion; manufacturing payrolls increased $4.8 billion, compared with anincrease of $1.5 billion. Services-producing industries' payrolls increased $17.8 billion, compared with an increase of $8.6 billion. Government wages and salaries increased $1.0 billion, in contrast to a decrease of $0.1 billion.

Transfer receipts, which are things like social security, has had no change for the last two months. Below is a graph of just transfer receipts.

Personal savings is disposable income minus outlays, or consumption and not adjusted for inflation. The Personal Savings Rate was 4.2% and in October was 4.5%.

To visualize more data from this report, consider playing around with more of the St. Louis Federal Reserve Fred graphs. Here are our overviews of personal income & outlays and overviews of GDP are here. This overview details the BEA Personal Income and Outlays statical release, which covers individual income, consumption and savings. The personal income & outlays report is annualized and seasonally adjusted, although most percentages are presented as monthly rates.

I wonder what it would be if the consumers that would be more

than happy to buy all the things they used to buy had any money to speak of?

Our expectations are so low now...